“Seven Reasons To Be Skeptical About SMRs (With Four Charts)”, By ROBERT BRYCE

“ Small modular reactors are promising. But commercializing them will be difficult and require staggering amounts of money. Only a few SMR companies will survive.”

Seven Reasons To Be Skeptical About SMRs (With Four Charts)

Small modular reactors are promising. But commercializing them will be difficult and require staggering amounts of money. Only a few SMR companies will survive.

Nvidia is on a tear. Its stock is up nearly 200% this year. The maker of semiconductors for AI is now worth some $3.3 trillion, making it one of the world’s most valuable companies.

That’s an impressive run. But the meme stock of the moment is NuScale Power. NuScale’s stock is up 844% this year, and a writer for the Motley Fool recently called it “unstoppable.”

The expected power demand for AI and the long-awaited boom in nuclear energy have NuScale and a slew of other SMR companies riding high. In March, Wood Mackenzie estimated the pipeline of SMR projects was worth more than $176 billion and that SMRs could account for as much as 30% of the global nuclear fleet by 2050. Earlier this month, Radiant Industries, which is developing a 1-megawatt reactor, raised $100 million in new funding. Meanwhile, several SMR companies, including TerraPower, Kairos, Natura Resources, and Oklo (whose stock has more than doubled this year), have all begun construction at their sites around the country.

That’s the good news. The less-than-good news is that, aside from NuScale, none of those companies have obtained approval for their reactor designs from the Nuclear Regulatory Commission. Furthermore, none of those SMR companies are profitable. NuScale lost $168 millionduring the first three quarters of this year. Oklo lost $63 million. (NuScale and Oklo have been targeted by short sellers. See here and here.)

Consider the case of Ultra Safe Nuclear Corporation (USNC). Last year, it was riding high. The company signed a joint venture agreement with Framatome, the French company that designs and produces components for nuclear power plants. The venture aimed to produce specialized (TRISO) fuel for USNC’s proposed 15-MW reactor. In announcing the deal, the CEO of Framatome, a subsidiary of Électricité de France, said it would help support the “rapid expansion of fourth-generation nuclear power.” On October 29, after burning through $200 million over the past three years, USNC filed for Chapter 11 bankruptcyin Delaware. Several other SMR companies are running low on cash. As one industry veteran told me, those companies “don’t have the wallets to make it happen.”

In short, the SMR sector looks frothy. There are simply too many companies and too many reactor designs competing in a brutal marketplace.

I first wrote about SMRs in 2008. In that article, which included a look at NuScale, I explained that small reactors may have applications “in remote areas where electricity is prohibitively expensive. They may also be used for temporary power production, or at locations like military bases that need highly reliable electric power.” And I said that several SMRs could be combined “to provide power for small cities that don’t need (or can’t afford) a much larger reactor.”

Those are the same claims we are hearing today. And yet, 16 years later, the US still hasn’t built a single SMR. Yes, we may be on the cusp of a nuclear comeback here in the US and around the world. I hope it happens. I’m adamantly pro-nuclear and have been for more than 15 years. But my first book, Pipe Dreams, published in 2002, was on Enron. Success in business depends on a company’s ability to produce cash. Why did Enron fail? It ran out of real money. And it’s cash — not necessarily the best technology — that will decide who will win the years-long, or rather, decades-long, contest to deploy SMRs in the US and around the world. In its bankruptcy filing, USNC said it failed because of “severe liquidity issues.” The liquidity required to get from the prototype and test stage (where nearly all of the SMR companies are now) to commercial deployment at scale, will likely be measured in billions of dollars

Energy realism requires sober analysis of all energy sources, not just the ones getting favorable headlines and stock valuations. One point before I continue: I don’t have a financial interest — either long or short — in any nuclear companies. Further, I’m not making any financial recommendations. As fellow Substacker Quoth The Raven says in his disclaimer, “I am an idiot and often get things wrong and lose money.”

With that out of the way, here are seven reasons to be skeptical about SMRs and a few ideas about what the incoming Trump administration and Congress should do to boost the US nuclear sector.

1) NextEra Energy, one of America’s most prodigious subsidy miners, isn’t convinced.

In October, John Ketchum, the CEO of Florida-based NextEra, said he was “not bullish” on SMRs. Ketchum said his company, the world’s biggest alt-energy producer, “has an in-house team dedicated to SMRs.” But that team has “not drawn favorable conclusions about the technology.” The article quotes Ketchum, who said many SMR companies are “very strained financially... There are only a handful that really have capitalization that could actually carry them through the next several years.” Ketchum also raised questions about the availability of nuclear fuel in the United States and noted that SMRs are “very expensive.”

NextEra has been ruthless in its pursuit of alt-energy subsidies. On several occasions, it has sued rural governments that have stood in its way. In 2013, it even sued a Canadian woman, Esther Wrightman for calling it “NexTerror” on her website. But it has also been disciplined in its approach. It has never invested in offshore wind because, as Ketchum explained last year, offshore turbines are subject to saltwater corrosion, the transmission issues are difficult, and the business is too capital intensive.

Since 2000, according to Good Jobs First, NextEra has collected nearly $3.4 billion in subsidies and another $5.4 billion in federal loans and loan guarantees. Among energy companies, only Sempra and NRG have collected more government handouts than NextEra. The company now has nearly $3.7 billion in tax credit carryforwards on its financial statements, which means it won’t pay much in federal taxes for years to come. When a company that excels at subsidy mining says it’s “not bullish” on SMRs, it may be worth paying attention.

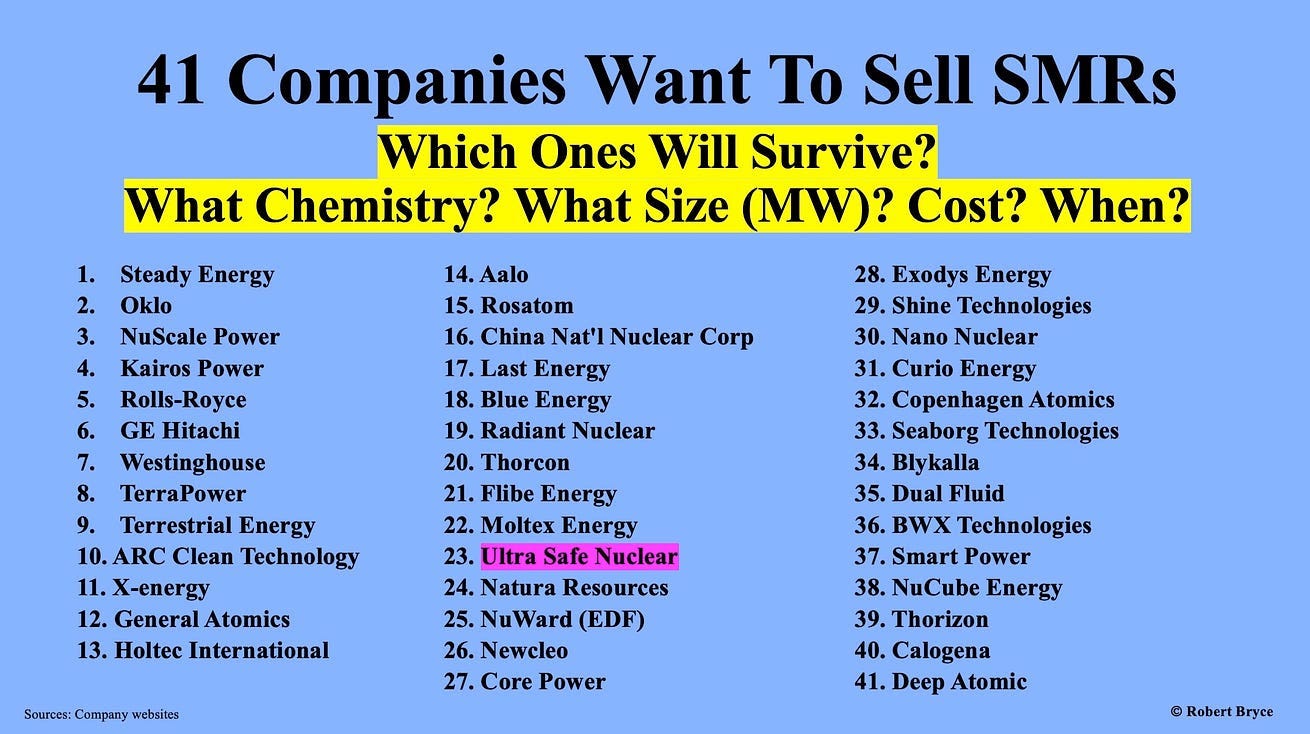

2) Way too many companies are trying to commercialize SMRs.

As seen above, at least 41 companies are vying to commercialize SMRs. (USNC is highlighted in purple.) Only a handful of them will survive. As one industry observer told me, “People don’t realize how hard it is to commercialize a new reactor.” TerraPower, which is backed by Bill Gates, will have enough money to see its first reactor built in Wyoming. Several other companies on the list are also going to survive, including ones that are owned or controlled by their governments, including Rosatom, NuWard, and China National Nuclear Corp. Diversified companies like Rolls-Royce, BWX Technologies, General Atomics, GE Hitachi (which is part of GE Vernova) and Holtec, are also going to survive. As for the others, it’s anyone’s guess as to which ones will be around in 10 years. Place your bets accordingly.

3) Regardless of the technology, building the first-of-a-kind SMR will be rocky and expensive.

Building the first copy of any complex machine — an automobile, boat, airplane, or nuclear reactor — is difficult and expensive. When the Utah Associated Municipal Power System agreed to have NuScale build a dozen of its SMRs at a site in Idaho, the cost was estimated at $4.2 billion. The project was canceled in late 2023 after the expected costs surged to $9.3 billion. Georgia Power’s experience at Plant Vogtle shows that gigawattt-scale reactors can have similar problems. Building the new reactors at Vogtle, Units 3 & 4, which use Westinghouse’s AP1000 design, took about seven years longer than projected. And when Unit 4 finally came online earlier this year, the cost of the reactors was about $17 billion more than expected. Given that track record, lenders and utilities will be leery about trying to build the next fleet of reactors, regardless of the size.

4) The regulatory environment is better, but it still costs too much and takes too long to get new reactors approved.

NuScale Power often reminds people that it has a licensed reactor that is ready to build. That’s true. But getting that approval from the NRC, which came in 2020, cost the company $500 million and took six years. And remember, NuScale’s reactor is a light-water reactor. That means its basic design is the same as the one used in the existing reactor fleet. SMRs that use different designs, such as gas cooled or molten salt, may face a more arduous permitting process. There are indications that the NRC is improving and moving faster to approve new designs. In addition, there’s increasing bipartisan support for nuclear energy on Capitol Hill and for keeping pressure on the agency. But the NRC still presents an unavoidable and unpredictable stumbling block. Until the NRC shows it can process new reactor designs promptly, the future of SMRs will be cloudy.

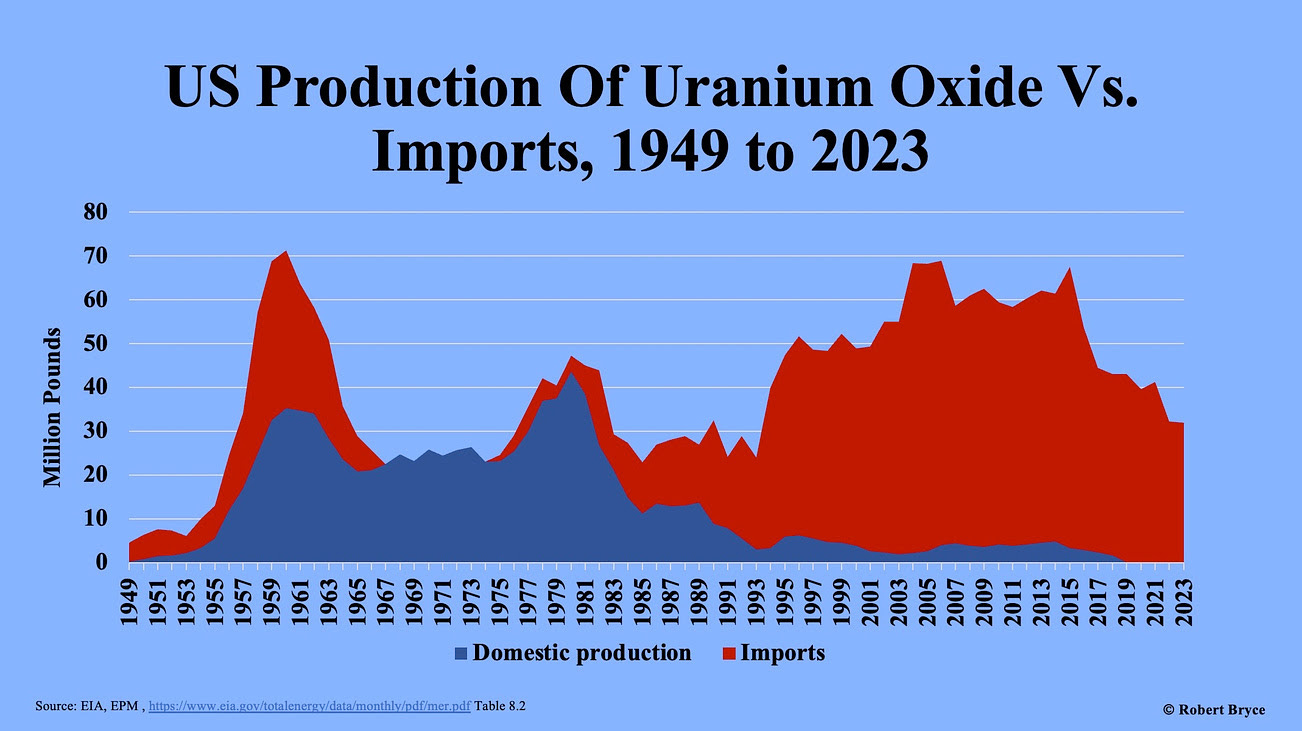

5) The US is too reliant on imported nuclear fuel, which means fuel availability and fuel cost will be challenging.

In October, the DOE released a report called “Pathways to Commercial Liftoff,” which said the US could triple its nuclear capacity to some 300 gigawatts by 2050. However, achieving that goal will require a massive increase in domestic mining and enrichment of uranium that can be turned into the fuel needed for the existing fleet of reactors and SMRs. As seen above, the US is now dependent on imported uranium. The DOE report says “Mining/milling of uranium will need to be increased from the US, allies, and partners to ensure a secure supply for the expected growth in nuclear capacity.” The problem is particularly obvious when it comes to enrichment. The DOE says the US will need access to about 50 million SWU, or separative work units, to produce enough nuclear fuel for that 300 GW of nuclear capacity. (A SWU is the effort required to increase the concentration of U235 in natural uranium. Obtaining higher levels of U235 requires more SWU.)

The DOE says the US now has about 4.4 million SWU, and its current demand for enriched uranium is about 15 million SWU. Thus, in rough terms, over the next three decades, the US will need three times more enrichment capacity than it has now.

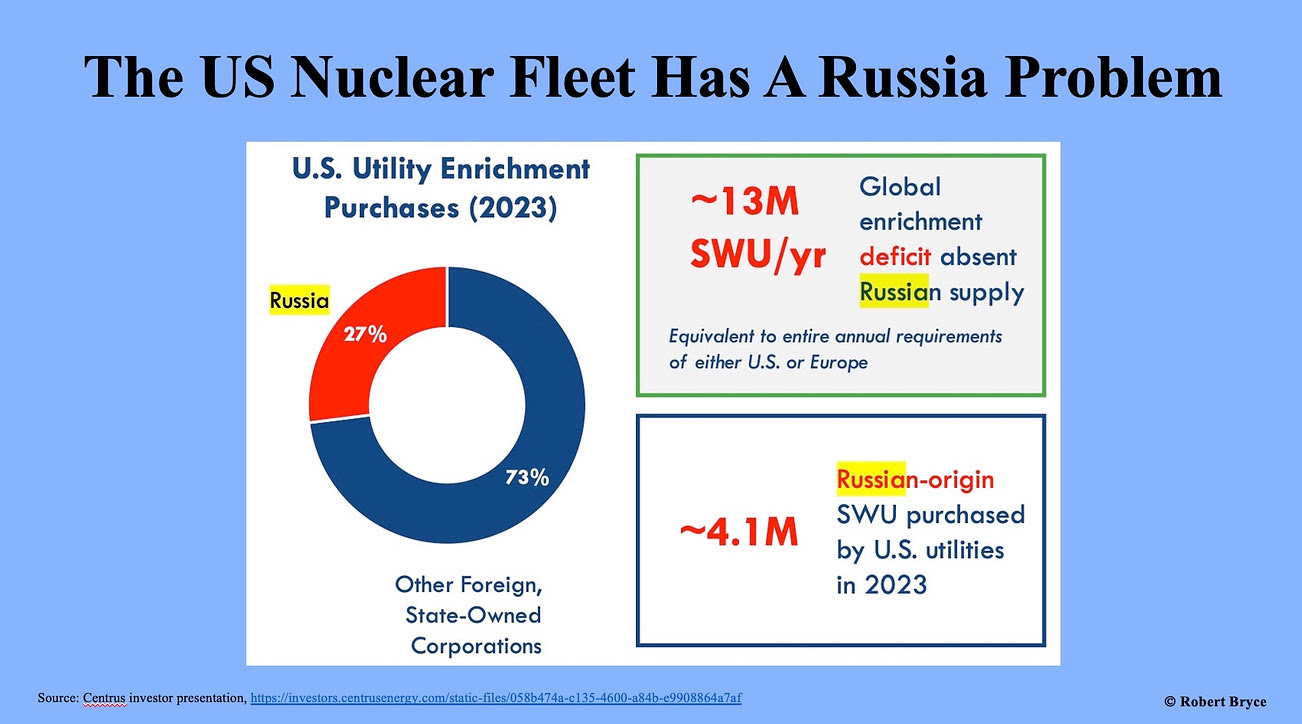

Russia’s invasion of Ukraine has further complicated the fuel supply challenge. As seen above, in 2023, 27% of the enriched uranium needed for the US nuclear fleet came from Russia. In May, President Biden signed into law the Prohibiting Russian Uranium Imports Act, which, as enrichment company Centrus Energy put it in its latest investor presentation, “effectively eliminates Russia as a competitor for enriched uranium in US post-2027.”

Many SMR companies hoping to commercialize their reactors need HALEU, which is short for high assay low enriched uranium. But the US is only producing tiny quantities of HALEU and producing it is expensive. Last year, Centrus, the only domestic producer licensed to produce HALEU, said that “A full-scale HALEU cascade, consisting of 120 individual centrifuge machines, with a combined capacity of approximately 6,000 kilograms of HALEU per year, could be brought online within about 42 months of securing the funding to do so.” But six metric tons won’t be nearly enough to meet demand. The Department of Energy has estimated that more than 40 metric tons of HALEU will be needed by 2030. It must also be noted that in 2022, TerraPower announced it was delaying the expected start date of its Natrium reactor project in Wyoming because it couldn’t get enough HALEU.

The only way to ensure that US reactors will have enough nuclear fuel in the decades to come is to build more mining and enrichment capacity here in the US. A source close to the enrichment sector told me the industry needs about $3 billion to build sufficient capacity. But that fuel enrichment will likely only be part of the total cost of building an integrated domestic nuclear fuel supply chain. (Note that I have not mentioned waste handling and disposal, which will also require long-term federal involvement.)

One final point on enrichment: a new company called Global Laser Enrichment recently acquired a site in Kentucky for a plant that aims to re-enrich some of the federal government’s depleted uranium stockpiles using lasers. The technology is far more efficient and cheaper than the current enrichment process, which uses centrifuges. If the laser technology works as expected, the Kentucky plant could become a significant source of domestic enriched uranium by the mid-2030s.

6) Security costs will be higher for SMRs than for large reactors.

About six years ago, I spoke to a top official at Georgia Power, which was dealing with delays in the construction of the new reactors at Plant Vogtle. (Those reactors are now online and producing power.) When I asked him about the future of SMRs, he gave a dismissive wave of the hand. When I asked why, he pointed to security costs and said something to the effect of, “Whether it’s 10 MW or 1,000 MW, you are going to need armed guards on staff to secure the power plant. And that’s going to be a major cost.” He continued, saying it's easier to spread the cost of armed guards over a power plant that is 1,000 MW or 2,000 MW than it is over a plant that’s 20 MW or 100 MW.

Are there technologies that can reduce those security costs? Perhaps. Motion-sensor devices, remote-controlled cameras, and other security systems can be deployed to keep SMRs safe from intruders. Security is a critical issue for nuclear plants that rarely gets mentioned in SMR discussions. But it isn’t going away.

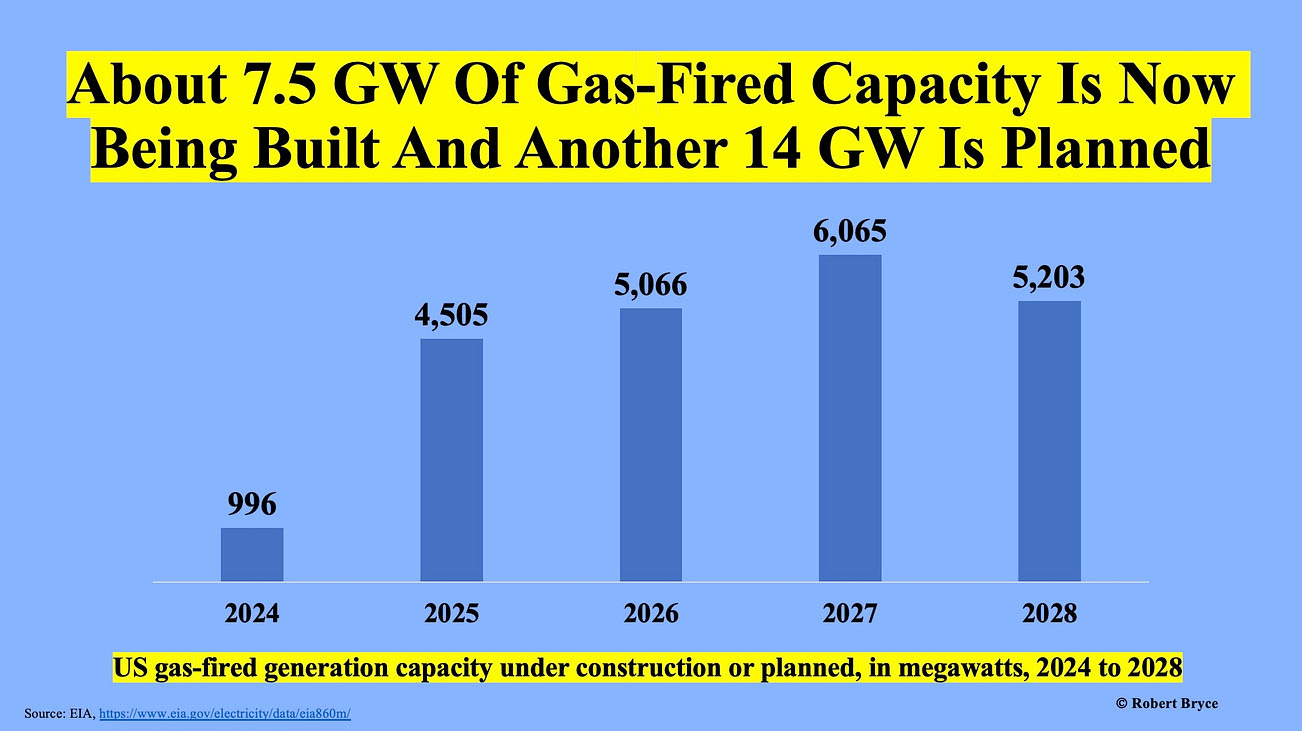

7) Gas-fired power plants, not nuclear, will meet near-term AI demand.

One of the factors driving the excitement about SMRs is the possibility that they will be used to power Big Tech’s data centers and the surge in electricity needed for AI. But by the time a substantial number of SMRs get licensed, built, and connected to the grid, which will likely take a decade, the AI boom may be over. Big Tech isn’t waiting around. Dozens of new gas-fired power plants are now being built across the country to meet that demand. That can be seen by looking at data published by the EIA.

As seen above, between now and 2028, some 21,800 MW of gas-fired capacity is currently under construction or planned and will be added to the US grid by 2028. That data comes from the agency’s latest Preliminary Monthly Electric Generator Inventory. To be clear, not all of that capacity, which includes steam turbines, combined cycle plants, combustion turbines, and internal combustion engines, will be built. Further, some of that capacity may be used as backup power, or for use as peaking plants, not as baseload power that data centers will need. Nevertheless, the EIA data shows that about 7,500 MW of gas-fired capacity is under construction and will come online by the end of 2026. The remaining 14,000 MW is waiting for regulatory approvals.

Those numbers may understate the growth in gas-fired generation. In April, the American Public Power Association reported that about 12,600 MW of gas-fired capacity has been permitted or is now under construction. And more capacity is being announced. Earlier this month, Facebook’s parent company, Meta, confirmed that it will spend $5 billion on a new data center project in Holly Ridge, Louisiana. The AI-focused data centers will be powered by gas-fired power plants owned and operated by Entergy, which has asked the Louisiana Public Service Commission to approve what it calls “a large and economically transformative facility.” According to Biz New Orleans, Entergy will build a 1,500 MW gas plant near the Meta site and another 754 MW plant will be built in southern Louisiana. Entergy expects to spend some $3.2 billion on the gas plants and related transmission capacity. The conclusion is obvious: when SMRs are ready to come online sometime in the next four or five years, gas-fired power plants may already meet much of the anticipated demand for data centers.

So what should happen next?

SMRs may eventually gain traction in the marketplace. But the hard reality is that there isn’t a single licensed reactor, of any size, under construction in the United States. That’s remarkable and disappointing. The US, which had led the nuclear age for decades, is now a laggard. And it’s a laggard at the same time that electricity demand for AI, heat pumps, and EVs is expected to surge over the next few years.

This could change if the Trump administration takes an aggressive stance on nuclear energy development. The president-elect is pro-nuclear. On Joe Rogan’s podcast, Trump even praised SMRs as a “potential answer” and said they may provide a way to “avoid the complexities associated with large reactors.” His nominee for Secretary of Energy, Chris Wright, knows the SMR sector well and has invested in it. Wright sits on Oklo’s board of directors. Given those facts, it’s reasonable to assume the new administration will be focused on reducing US dependence on nuclear fuel from Russia and on how it can develop more domestic enrichment capacity.

About 18 months ago, I wrote a piece on the nuclear fuel challenge, “No U,” in which I suggested that Congress should “formulate a comprehensive national industrial policy focused on nuclear energy.”

Congress should also implement an idea put forward by the sharp-eyed energy analyst Matt Wald. In an article published last year by the American Nuclear Society, Wald said the US should create the nuclear equivalent of the Strategic Petroleum Reserve so the domestic nuclear fleet is assured of fuel security. (I interviewed Wald on the Power Hungry Podcast last year. You can listen to it here.) Wald pointed out that the federal government has a myriad of programs that help protect the country’s overall security including the SPR, flood insurance, and price supports for agricultural commodities. The government should do the same by creating a system that assures stable prices for uranium, conversion, and enrichment. To achieve that, Congress should fund a program that establishes a floor price for enriched fuel so domestic producers can be assured that the bottom won’t fall out of the market and leave the owners of enrichment facilities with worthless assets. Congress should also reduce permitting obstacles for domestic uranium mines and establish a floor price for domestically mined uranium.

In short, there’s no scenario under which the US nuclear sector thrives that doesn’t include a substantial increase in federal support for nuclear energy. As Wald concluded in his article, the events of the past few years, combined with Russia’s invasion of Ukraine, have created a “new consensus: that institutions bigger than corporations — namely, governments — should be involved.”

As a candidate, Donald Trump talked extensively about American energy. During his second term, Trump and his appointees could make a real difference to our future energy security by nurturing the domestic nuclear sector. Doing so will help fortify our electric grid, which has been fragilized by lousy policy and inattention. Excessive subsidies for weather-dependent sources like wind and solar are weakening the grid, which now relies too heavily on power plants that rely on just-in-time deliveries of natural gas. Affordable, reliable, and resilient electricity systems should be considered a national security imperative. A robust nuclear sector, one that deploys large reactors and SMRs alike, would help turn that imperative into a reality.

eVinci is definitely a consideration for vSMRs.

The uranium enrichment issue in the US could potentially also be alleviated if they would embrace CANDU technology since it uses U-235 natural unenriched uranium instead.

CANDU 600MW modular reactors have been deployed in some areas of the world already, and, there is also talk of a CANDU SMR (CSMR) with a 300MW capacity. All using natural unenriched uranium.

Meanwhile in Canada; "The Saskatchewan Research Council (SRC) and Westinghouse Electric Canada have signed a Memorandum of Understanding (MOU) to advance very small modular reactors (vSMRs), also known as micro-reactors, in Saskatchewan. "SRC is no newcomer to nuclear power, having operated a SLOWPOKE-2 nuclear reactor for about 40 years." Westinghouse says the eVinci microreactor is expected to have its design certification in 2027 and the first construction to begin in 2030. From Westinghouse; "The eVinci microreactor has very few moving parts, working essentially as a battery, providing the versatility for power systems ranging from several kilowatts to 5 megawatts of electricity, delivered 24 hours a day, 7 days a week for eight-plus years without refueling. It can also produce high temperature heat suitable for industrial applications including alternative fuel production such as hydrogen, and has the flexibility to balance renewable output. The technology is 100 percent factory built and assembled before it is shipped in a container to any location." Westinghouse already has nuclear assets that are strategic, proven, licensed and permitted. There is no cause for concern regarding the viability of the Westinghouse Electric Company.