What the ‘Streisand Effect’ has to with climate investing Anti-ESG backlash is actually increasing investor interest

What the ‘Streisand Effect’ has to with climate investing Anti-ESG backlash is actually increasing investor interest

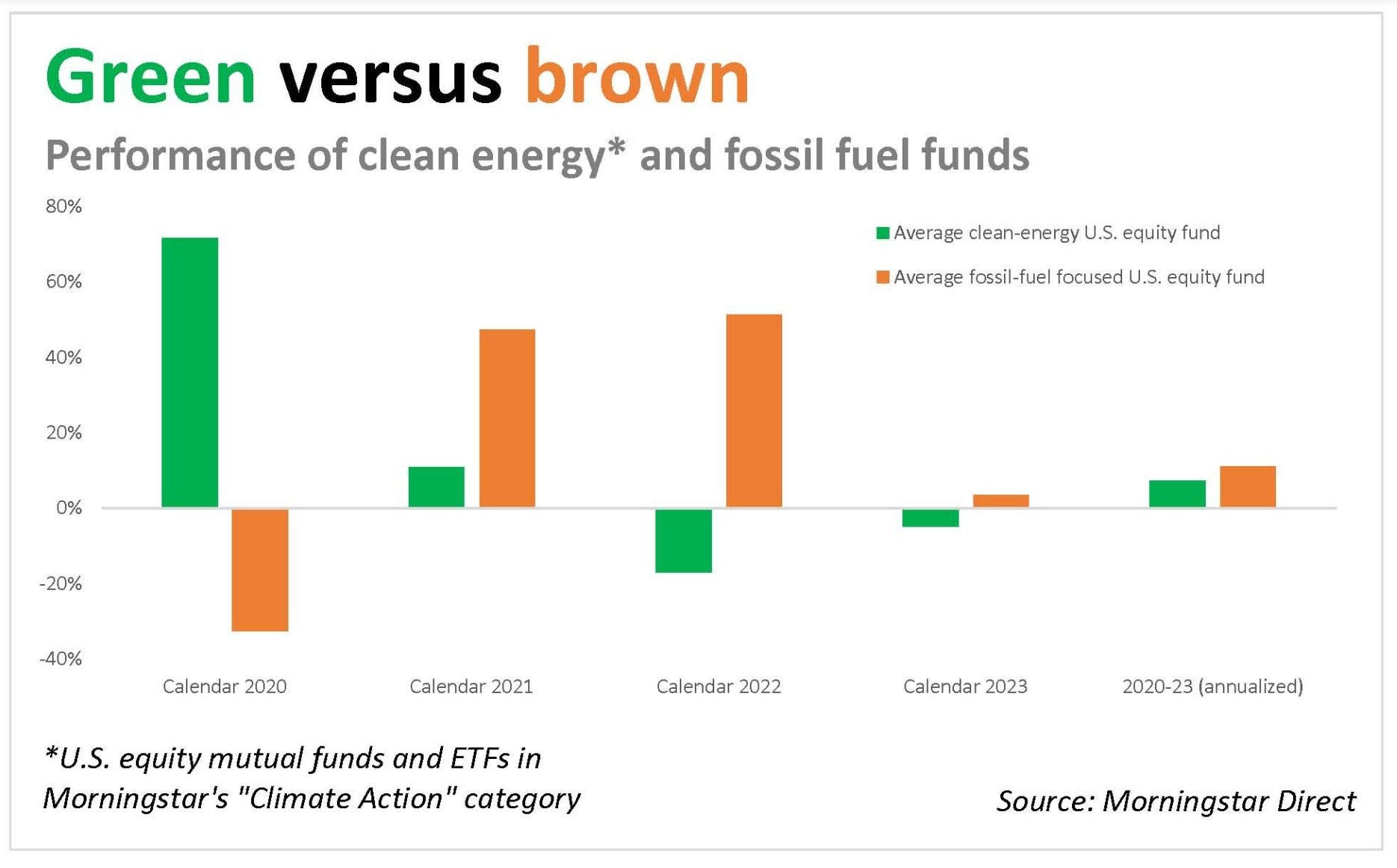

CHAPEL HILL, N.C. (Callaway Climate Insights) — Last year was the third in a row in which climate-focused funds significantly lagged those that invest in fossil fuel companies. It wasn’t close

(Mark Hulbert, an author and longtime investment columnist, is the founder of the Hulbert Financial Digest; his Hulbert Ratings audits investment newsletter returns.)

The average climate-focused fund lagged the average fossil fuel fund by more than eight percentage points — as you can see from the accompanying chart. Perhaps the only solace climate-friendly investors can find in the 2023 results is that climate-focused funds didn’t do even worse. The margin by which they lagged fossil fuel funds in 2022 was a huge 67 percentage points; in 2021 they lagged by 58 percentage points.

These averages are derived from data provided by Morningstar Direct. The climate-focused average was based on those U.S. equity funds (both open-end and ETFs) that Morningstar includes in its “Climate Action” category. That “includes strategies focused on investing in companies or projects that contribute broadly to the transition to a low-carbon economy.” The fossil-fuel fund average, in contrast, was based on those funds in Morningstar’s “Equity Energy” category that are not included in its “Climate Action” category.

Climate funds’ underperformance over the past three years more than offsets their huge outperformance in 2020. That was the banner year for climate-friendly funds, of course, when on average they outperformed fossil-fuel funds by more than 105 percentage points. When that year’s results are combined with those over the subsequent three years, however, the average climate-focused fund lags by 3.7 annualized percentage points.

The green discount

This 3.7 percentage point difference may very well be a good estimate of the green discount in coming years — the extent to which climate funds (aka green funds) will lag fossil fuel funds (aka brown funds). The reasons for this discount are well known to readers of this column, so I will only briefly summarize.

By favoring green companies over brown ones, climate-focused investors are lowering the former’s cost of capital and increasing the latter’s. As Finance 101 teaches us, the long-term return of a company’s stock should equal its cost of capital. Climate-focused investors therefore should expect the average green company stock to lag the average brown company stock over the long term.

That’s the theory, and stock market history provides considerable support for it. Consider the long-term performance of tobacco industry stocks in the U.S., which have been shunned by socially responsible investors for perhaps longer than those of any other industry — for over a century. This has boosted these companies’ cost of capital and, sure enough, their long-term returns. According to the Credit Suisse Global Investment Returns Yearbook 2020, one dollar invested in the U.S. market in 1900 would have grown to $58,191 by 2020. In contrast, one dollar invested in the tobacco industry grew to more than $8 million.

The good news

Fortunately, it appears as though investors are not losing interest in climate-friendly stocks, even as fossil fuel stocks are performing much better. Their resolve is particularly noteworthy, given the intense political backlash that ESG investing has received in recent years, spearheaded by Florida Gov. Ron DeSantis and Texas Gov. Greg Abbott. That backlash has gathered steam in recent years as climate-friendly stocks and funds have lagged fossil fuel companies.

A recent Bloomberg Intelligence survey of institutional investors and top corporate executives found that the overwhelming majority remain committed to ESG, however. 54% of respondents said that the political backlash has led them to focus even more on ESG than they were before.

Joachim Klement, a trustee of the CFA Institute Research Foundation and Head of Strategy at Liberum Capital, recently reviewed the results of the Bloomberg survey, commenting that the “political pushback is not only going nowhere but suffers from the ‘Streisand effect’.” He is referring to what happened in 2003 after Barbra Streisand tried to suppress a photograph of her Malibu mansion that illustrated coastal erosion. As Wikipedia puts it, her efforts “inadvertently drew far greater attention to the previously obscure photograph.”

How ironic